Month-End Is Broken for Most Finance Teams

Most finance teams close the month with a sense of completion. The numbers are in, the reports are shared, and the P&L is reviewed. Revenue, costs and margins are all laid out clearly. On the surface, it looks like a disciplined process.

But very little insight is actually created.

In many businesses, there is no real variance analysis taking place. Often, there is not even a proper budget or a detailed enough monthly P&L to compare against. Companies operate with a rough understanding of what they earn and what they spend, but without a clear baseline, there is no way to assess performance. This is one of the most common issues we see when starting work with new clients, and it is also where the biggest opportunities tend to sit.

Because the reality is simple. What gets tracked gets better. And most businesses are not tracking their performance in a way that allows them to improve it.

No Budget, No Visibility, No Control

A lot of companies do not skip variance analysis because they choose to. They skip it because they cannot do it.

Without a structured budget and a detailed monthly P and L, there is nothing to compare actual performance against. Finance teams are left with a general sense of how the business is performing, but no clear way to measure whether results are better or worse than expected. This creates a reactive environment where decisions are based on instinct rather than evidence.

This is where the frustration comes in. Especially in growing businesses, there are always low hanging opportunities to improve performance. Redundant costs, inefficient spend and underperforming areas exist in almost every organisation. But without proper tracking and comparison, these issues remain hidden. The moment you introduce structure and start measuring variances, these quick wins become visible and actionable.

We worked with a technology services company that could not reach profitability, regardless of how much revenue it generated. From the founder’s perspective, the issue was clear. They believed the business simply was not selling enough, so the focus was on increasing ARR and bringing in more contracts.

But the results did not improve.

Once we introduced a proper budget and structured the P and L in a way that allowed for variance analysis, the picture changed quickly. Instead of looking at totals, we broke costs down into meaningful categories and started tracking deviations month by month. What emerged was a completely different narrative.

There were tools and subscriptions that were either underused or not needed at all. Marketing spend and commission structures were not translating into revenue. Margins were too low to ever support a profitable model. None of this was visible before. The variance analysis acted as a magnifying glass, giving the business a level of clarity and granularity it simply did not have access to.

Variance analysis on its own is not enough. The real value comes from linking financial movements to what is actually happening inside the business.

In practice, most cost categories should not be analysed in isolation. Wages and salaries, for example, only become meaningful when viewed alongside time tracking data. This is what allows you to understand project profitability and how efficiently your team is being deployed. In the same way, marketing and advertising spend should feed directly into CAC, while gross and operating margins should be interpreted in the context of delivery efficiency.

This is where finance moves beyond reporting and starts becoming operational. Instead of simply explaining movements in numbers, it explains how the business is functioning. Without this connection, variance analysis remains surface level. With it, it becomes a tool that drives real understanding and better decisions.

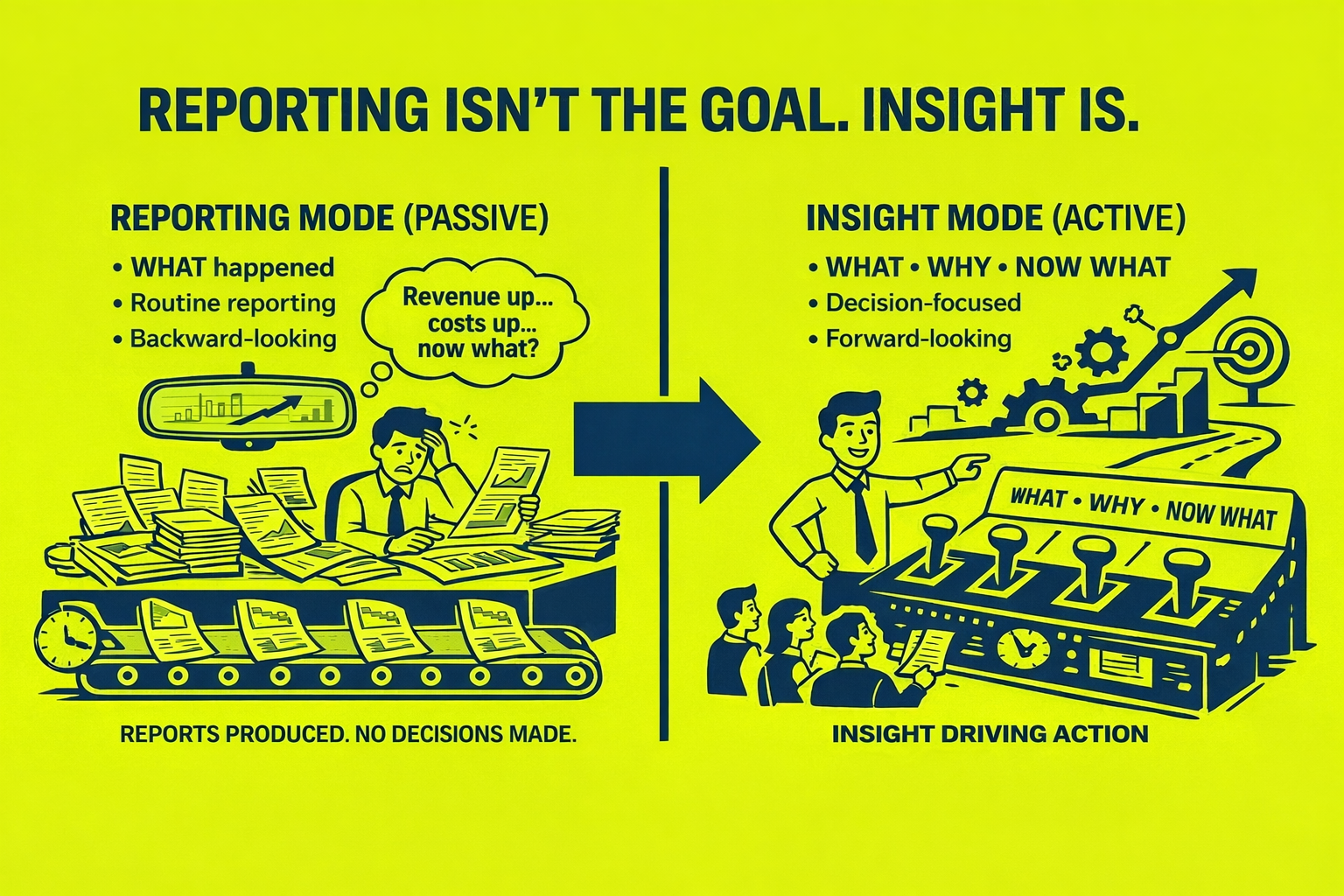

From Reporting to Insight

Creating a variance analysis today is not difficult. With modern tools and AI, most finance teams can produce reports quickly and with a high level of accuracy. The barrier is no longer technical.

The difference lies in how the analysis is used.

A good variance analysis will tell you what happened. It will show that revenue is up or down, or that costs have increased against budget. But a great variance analysis goes further. It answers three critical questions. What happened, why it happened, and what that means for the business going forward.

This is where most companies fall short. The process becomes a routine exercise, a set of numbers reviewed at month end without any real interpretation. But when done properly, variance analysis should drive a conversation. It should shape decisions, challenge assumptions and provide a clear direction on how the business needs to move to achieve its goals.

The most common issue we see is not a lack of data. It is how that data is communicated.

Most variance analyses simply describe what happened. You will see statements like revenue is five per cent below budget or costs are slightly higher than expected. While technically correct, this does not add much value to the business.

What is missing is the explanation.

Why is revenue below budget. Is it due to fewer deals, lower pricing, or delays in delivery. Is the impact short term or something more structural. What does it mean for cash flow, hiring plans or growth targets. Without this layer of interpretation, the analysis does not lead anywhere.

If there is one thing to fix in most month end processes, it is this. Add a few lines of clear commentary to every major variance. Explain the drivers and explain the implications. That small shift turns variance analysis from a reporting exercise into a decision making tool.

Why Variance Analysis Should Sit at the Core of Finance

When variance analysis is done properly, it changes the role of the finance function entirely.

It shifts finance away from simply reporting historical numbers and positions it as a driver of decisions. Instead of looking backwards, the focus moves towards understanding what the numbers mean and how the business should respond. This creates a much stronger link between finance and the rest of the organisation, as insights start to influence actions across teams.

It also introduces a level of accountability that is often missing. When variances are clearly explained and connected to operational drivers, it becomes easier to identify where performance is strong and where it needs attention. Over time, this improves forecasting, highlights risks earlier and allows the business to act with more confidence. Finance stops being a passive function and becomes an active part of how the business moves forward.

If your month end process currently stops at reporting, there is a clear opportunity to get more out of your numbers. At Quantro, we work with businesses to implement structured variance analysis that goes beyond the surface, uncovering inefficiencies, improving margins and turning finance into a true decision making function. You can book a call with us to see how this would look in your business.

More from Quantro

Innovative cash flow management strategies are crucial for any business's survival and growth. In this blog, we cover optimising payment cycles, using financial tools for passive income, leveraging technology for real-time insights, and building a cash-savvy culture. The article provides practical advice, aiming to transform routine financial management into a strategic asset that enhances operational efficiency and financial stability, equipping businesses to navigate complex economic landscapes effectively.

Read More →Explore the complexities of scaling operations in service businesses. We look into recognising the right time to scale, addressing operational challenges, leveraging technology efficiently, maintaining exceptional customer experience, and managing team dynamics effectively. We use practical examples of how to use key performance indicators to navigate growth and ensure that your business not only expands in size but also enhances its capabilities and maintains its core values. Perfect for business leaders seeking to understand the nuances of sustainable growth in the service sector.

Read More →