When Profit Looks Good but the Business Still Feels Uncertain

Profit is an important indicator of business performance. It shows whether a company is creating value over time, whether pricing decisions are broadly effective, and whether costs are being managed with discipline. For many small companies, profit is the primary reference point for assessing how well the business is doing.

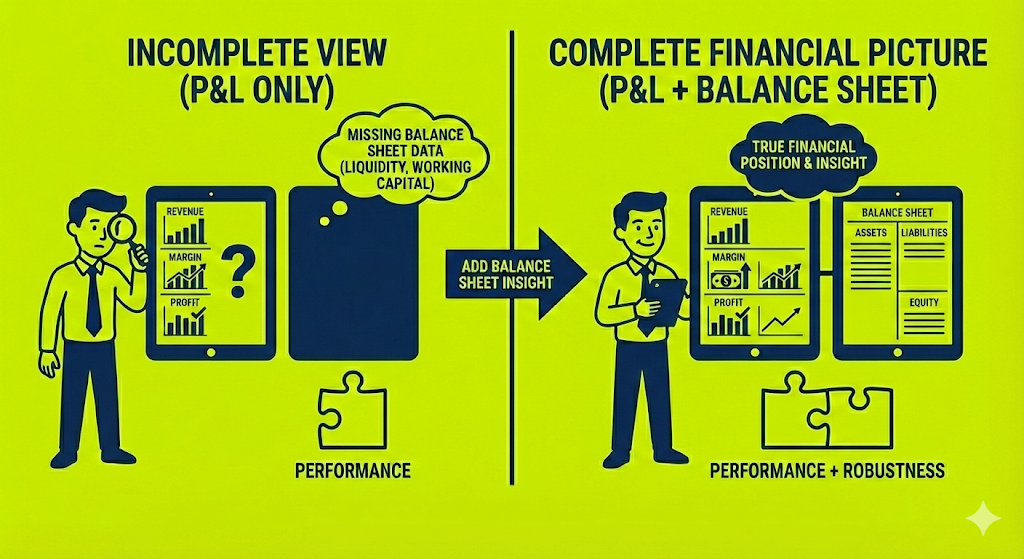

However, profit on its own does not describe the full financial reality of a company. It does not explain how much cash is available to fund day to day operations, how exposed the business is to short term obligations, or how resilient it would be under unexpected pressure. A business can report consistent profits while operating with limited financial flexibility.

This is where uncertainty often enters the picture. Founders may see positive results on their profit and loss statement, yet still hesitate when it comes to hiring, investing, or committing to growth. Without visibility beyond profit, decisions feel harder to justify. The balance sheet provides the missing context, showing not only how the business has performed, but how well it is positioned to support the next decision.

One of the most striking patterns we see when working with small companies is how little attention is paid to the balance sheet. In many cases, it is not actively reviewed at all. Founders track revenue, margins and profit, but they do not measure liquidity, gearing or working capital in any meaningful way. This means a valuable set of indicators is simply missing from the decision making process.

Without balance sheet data, it becomes almost impossible to understand the true financial position of the business. A company can appear successful on its profit and loss statement while quietly building risk on the balance sheet. Cash may be tight despite reported profits, liabilities may be increasing faster than assets, or short term obligations may be approaching without a clear plan to meet them. These issues rarely show up in isolation. They are usually connected and they tend to surface only when pressure is already high.

By overlooking the balance sheet, founders are not just missing numbers. They are missing insight. The balance sheet completes the story that the profit and loss statement starts. Together, they explain not only how the business performed, but how robust it actually is. Ignoring one while relying on the other leads to an incomplete and often misleading view of performance.

Profit is designed to measure economic performance over time. It tells you whether the business model works, whether pricing covers costs, and whether value is being created. As a metric, it is excellent at answering the question of performance. It is far less effective at answering questions of timing, risk, and financial flexibility.

Those questions sit elsewhere. They live in how quickly customers pay, how much capital is tied up in operations, and how obligations accumulate on the other side of the balance sheet. None of this contradicts profitability. In fact, many of the businesses that struggle most with financial pressure are profitable ones whose operational structure absorbs cash faster than it releases it.

This is why the balance sheet is essential for translating performance into control. It shows how profit interacts with reality, how value creation turns into liquidity, and where friction quietly builds up inside the business. When founders understand these relationships, financial pressure stops being abstract. It becomes something that can be addressed through concrete operational choices.

When reviewed properly, the balance sheet offers clear guidance on where a business should focus its efforts. It does not just describe the current state of the company. It points directly to the areas creating pressure and, just as importantly, to the actions that can relieve it. This is why we place so much emphasis on understanding the relationships between assets and liabilities, rather than looking at individual line items in isolation.

Metrics such as working capital, the current ratio, the quick ratio and the cash ratio quickly surface underlying issues. They show whether the business can comfortably meet its short term obligations, how dependent it is on future cash inflows, and how much room it has to manoeuvre. These indicators often reveal problems long before they become visible in the profit and loss statement.

For many founders, simply starting to look at these measures is a turning point. Instead of reacting to financial stress as it appears, they gain a framework for prioritisation. The balance sheet becomes a map. It shows where risk is accumulating and where small, focused changes can have a disproportionate impact on stability and growth.

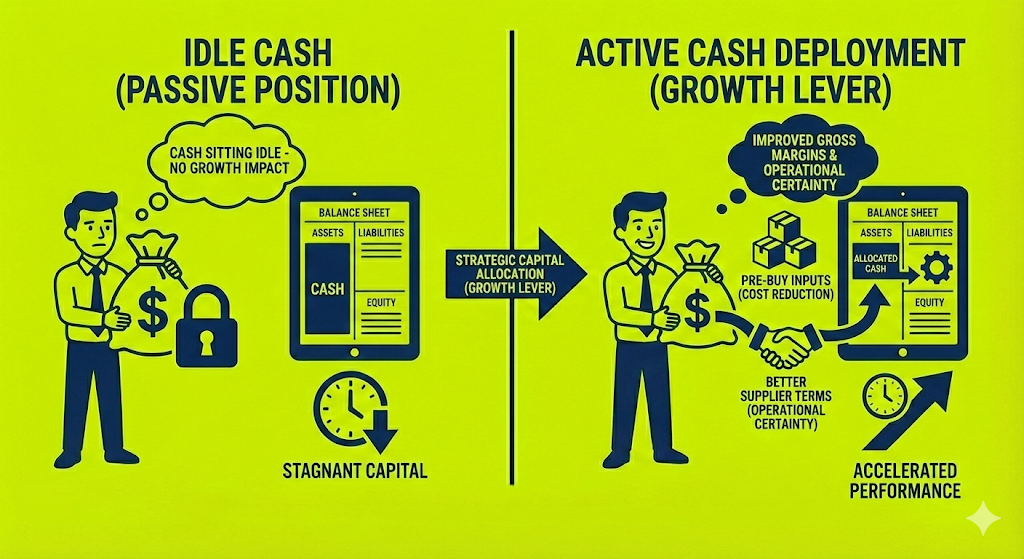

In one case, we worked with a client whose business was profitable and cash generative. Their balance sheet showed a strong cash position, which initially felt reassuring. However, when we looked more closely, it became clear that a large portion of that cash was simply sitting idle. It was not allocated with intent, and it was not actively supporting the company’s growth.

To understand this better, we focused on two simple measures. The first was the cash to expense ratio (benchmark 2x for fast growing businesses, 3x for scaling businesses), which showed how many months of operating costs the company was holding in cash. The second was the current ratio (benchmark 1.5x), calculated as current assets divided by current liabilities, which helped us assess how comfortably the business could meet its short term obligations. Together, these metrics made it clear that the company had more liquidity than it needed for stability, but no clear plan for how that liquidity should be used. This highlighted an opportunity to use existing cash more effectively rather than keeping it untouched. The decision was made to pre buy core inputs and negotiate better terms with suppliers, reducing cost volatility and strengthening operational certainty.

The impact was immediate and meaningful. Gross profit margins improved significantly, not because revenue increased, but because the balance sheet was put to work. This is a good example of how reviewing the balance sheet does not only protect downside risk. When used deliberately, it can actively create growth and improve performance across the business.

At Quantro, we do not treat the balance sheet as something separate or secondary to the profit and loss statement. We review it on a monthly basis, with the same discipline and attention. This is intentional. Financial clarity only comes when performance and position are understood together, not in isolation.

Our key metrics are therefore a combination of profit and loss and balance sheet indicators. Margin trends are reviewed alongside working capital movements. Cash performance is assessed in the context of liabilities and upcoming obligations. By looking at both sides at the same time, patterns emerge much earlier and decisions become more grounded in reality.

This approach turns the balance sheet into an active management tool. Rather than reacting to issues once they appear in cash flow, founders gain visibility into where pressure is building and where flexibility exists. Over time, this creates a calmer and more deliberate way of running the business, where growth decisions are supported by structure rather than gut feel.

Most founders do not start companies because they enjoy financial reporting. They build businesses because they care about the work, the product, or the value they create for their clients. Financial stress often appears not because the business is failing, but because there is a lack of clarity around what is really happening beneath the surface.

Profit shows how a business has performed over a period of time. The balance sheet shows how strong and resilient it is today. When both are reviewed and understood together, decision making becomes calmer and more confident. Investments feel intentional. Growth feels supported by structure rather than driven by pressure.

For small companies, this shift can be transformative. Treating the balance sheet as a strategic tool rather than an afterthought allows founders to keep doing what they do best, while building a business that is financially stable and ready for the next stage of growth. If you want to understand what your balance sheet is really telling you, and how to use it alongside your profit and loss to make better decisions, we are always happy to start with a conversation.

More from Quantro

Innovative cash flow management strategies are crucial for any business's survival and growth. In this blog, we cover optimising payment cycles, using financial tools for passive income, leveraging technology for real-time insights, and building a cash-savvy culture. The article provides practical advice, aiming to transform routine financial management into a strategic asset that enhances operational efficiency and financial stability, equipping businesses to navigate complex economic landscapes effectively.

Read More →Explore the complexities of scaling operations in service businesses. We look into recognising the right time to scale, addressing operational challenges, leveraging technology efficiently, maintaining exceptional customer experience, and managing team dynamics effectively. We use practical examples of how to use key performance indicators to navigate growth and ensure that your business not only expands in size but also enhances its capabilities and maintains its core values. Perfect for business leaders seeking to understand the nuances of sustainable growth in the service sector.

Read More →